{kind=link}

Crypto merchants have turned Elon Musk’s anticipated SpaceX itemizing right into a round the clock proxy market, pushing greater than $1 billion by means of SpaceX-linked perpetual futures within the final three days as traders attempt to front-run one of many largest public choices in Wall Road historical past.

The shift comes as retail traders face restricted allocations in a closely oversubscribed providing and search for different methods to achieve publicity.

It additionally arrives with a warning from market historical past as a few of the most celebrated know-how listings of the previous decade opened to huge demand, solely to punish early patrons with steep first-year losses earlier than settling into longer-term buying and selling patterns.

Crypto turns into the early buying and selling flooring

Earlier than SpaceX shares start buying and selling on a standard trade, crypto venues have change into the closest factor to a stay marketplace for the corporate’s anticipated public debut.

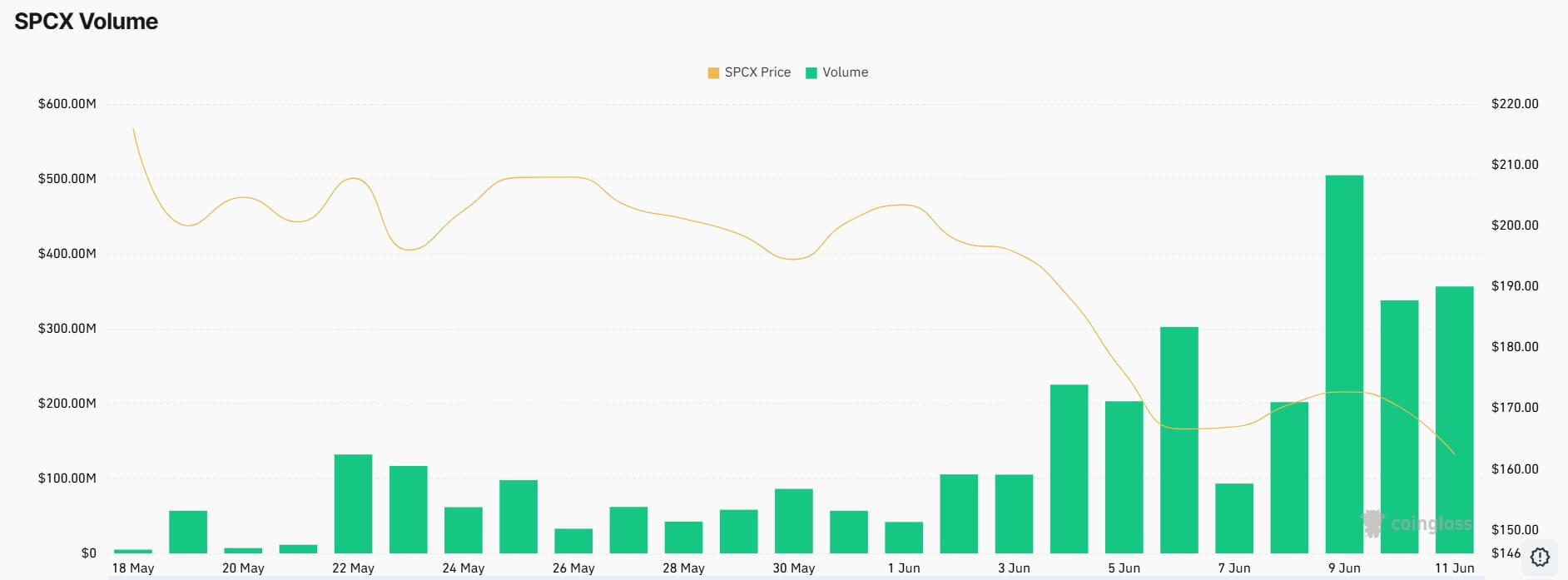

The SPCX perpetual future, an artificial contract linked to SpaceX’s pre-IPO valuation, has drawn greater than $1 billion in buying and selling quantity over the previous 72 hours, CoinGlass knowledge present. Since Might 30, cumulative quantity throughout taking part platforms has exceeded $2.6 billion, with open curiosity round $363 million.

In contrast to unusual fairness choices, perpetual futures don’t have any expiration date. Merchants can maintain positions indefinitely, however they have to handle funding funds and the danger of liquidation if costs transfer sharply in opposition to them.

That construction makes the market particularly engaging to crypto merchants accustomed to excessive leverage and steady worth motion.

Hyperliquid helped pioneer the SPCX contract, however exercise has since unfold past decentralized finance. Binance, the world’s largest crypto trade by buying and selling quantity, now accounts for a big share of the market, displaying how shortly an artificial product can change into a serious venue for worth discovery earlier than the underlying inventory exists in public markets.

In the meantime, the market is attracting bullish bets. Arkham Intelligence stated one dealer utilizing the deal with “wenyu8888888” had positioned a $5.7 million, 2x quick on SPCX, describing it as the biggest SpaceX quick it had tracked.

The place highlights how the artificial market has additionally change into a venue for merchants keen to wager that the IPO premium will fade as soon as public buying and selling begins. It additionally exhibits how shortly a single leveraged account can change into a part of the broader spectacle across the itemizing.

For merchants shut out of the official bookbuild, the contract provides a approach to specific a view on SpaceX earlier than the opening bell.

For market watchers, it provides one thing Wall Road’s formal IPO course of doesn’t: a constantly transferring worth backed by actual capital, leverage, and liquidation danger.

That makes the SPCX market a tough however helpful gauge of speculative urge for food, because it exhibits the place merchants keen to take fast monetary danger imagine the inventory may commerce as soon as public markets get their first likelihood to cost it.

Nonetheless, it doesn’t grant possession in SpaceX, voting rights, or any declare on shares.

The premium remains to be there, however smaller

The futures market continues to counsel that merchants count on SpaceX to open above its reported IPO worth.

The corporate’s providing has been priced at $135 a share, giving SpaceX an anticipated valuation of roughly $1.75 trillion to $1.8 trillion. At about $162, the SPCX contract implies a premium of roughly 17% to the itemizing worth.

Whereas that represents a significant hole, it’s also a pointy reset from the early days of the contract, when speculative shopping for drove costs above $220 and, at one level, close to $230.

At these ranges, merchants have been pricing in a far bigger first-day leap and treating SpaceX as a shortage asset earlier than its inventory turned broadly obtainable.

The compression in that premium is necessary as a result of it exhibits the market has change into extra selective at the same time as headline demand stays huge.

Underwriters have drawn a whole bunch of billions of {dollars} in investor curiosity for a deliberate $75 billion increase, making the deal a number of instances oversubscribed.

In lots of IPOs, that sort of demand would enable bankers to raise the ultimate worth vary earlier than shares start buying and selling. SpaceX’s fixed-price construction leaves much less room for that adjustment, forcing traders to just accept the $135 worth or stroll away.

Retail demand has added one other layer of stress. SpaceX reserved a larger-than-usual portion of the providing for particular person traders, however the scale of demand means many patrons are prone to obtain solely a part of what they requested.

A few of that pissed off demand seems to be spilling into artificial markets, the place merchants can construct publicity instantly however tackle dangers that differ markedly from these of proudly owning frequent inventory.

IPO historical past offers patrons motive to pause

The push for SpaceX publicity is operating right into a warning from the current historical past of main know-how listings: even sturdy corporations can ship painful early returns when traders purchase at aggressive valuations.

Charlie Bilello, chief market strategist at Inventive Planning, has argued that one frequent mistake traders make throughout high-profile listings is treating an important enterprise as an important funding at any worth.

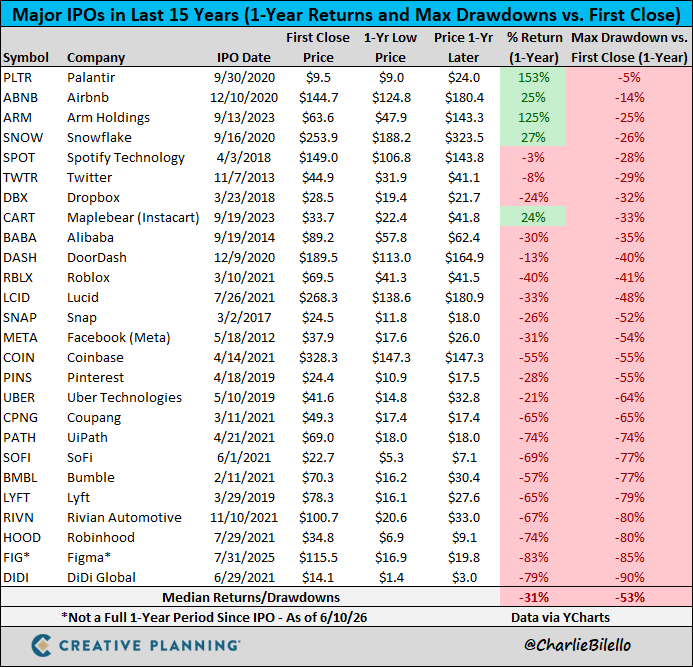

His evaluation of main IPOs exhibits that the median providing loses 31% in its first 12 months and suffers a peak-to-trough drawdown of 53% alongside the best way.

That time has change into extra related as some traders examine SpaceX, OpenAI, and Anthropic with the early public-market days of Amazon, Google, and Meta. They argue that purchasing the following era of dominant know-how corporations at IPO may resemble shopping for the final era of web giants earlier than they turned a few of the most dear companies on the earth.

Nonetheless, Jim Chanos, the veteran quick vendor, rejected that comparability and argued that the valuation hole is simply too massive to disregard.

Based on him, Amazon went public in 1997 at a valuation of about $450 million, or roughly thrice income. Google was listed in 2004 at about $23 billion and roughly seven instances income. Meta debuted in 2012 at a valuation of about $104 billion and round 20 instances income, then bought off sharply after itemizing.

Chanos argues that SpaceX is ranging from a valuation that already dwarfs these early public-market entry factors, leaving much less room for traders to learn from a number of enlargement if development falls wanting the market’s most aggressive expectations.

He additionally pointed to Uber as a cautionary instance of how massive addressable-market forecasts can fail to translate instantly into public-market worth. Uber pitched a complete addressable market of greater than $12 trillion when it went public in 2019. Its market capitalization is now about $150 billion, a bit of over 1% of that projected alternative.

Utilizing the same method, Chanos argued, would indicate a a lot decrease worth for SpaceX than the roughly $2 trillion stage now being mentioned by the market.

Thierry Borgeat, co-founder of the monetary analysis agency Arvy, reached the same conclusion after monitoring the post-listing efficiency of outstanding know-how and development corporations over the previous decade.

Based on him, the document exhibits that first-year volatility has been the rule, even for corporations that later turned main market winners.

For context, Fb fell 54% from its first-year excessive earlier than recovering. Snap, Uber, Pinterest, Lyft, Rivian, and Robinhood suffered even deeper drawdowns, with declines starting from 56% to 90% throughout their first 12 months as public corporations.

Based on Borgeat, the sample was not confined to damaged listings. Zoom Video Communications completed its first 12 months up 142%, however solely after enduring a 40% drawdown. Palantir Applied sciences closed its first public 12 months up 153%, whereas nonetheless forcing early holders by means of a 53% decline earlier than the rebound took maintain.

Moreover, CrowdStrike, Datadog, and MongoDB additionally ended their first 12 months in constructive territory, however every skilled sharp interim declines.

The lesson from these listings is that early demand can raise a inventory on debut with out stopping a extreme reset as soon as the market begins testing valuation, development assumptions, and investor persistence.

That historical past complicates the present SpaceX commerce. Crypto derivatives nonetheless counsel merchants count on the corporate to open above its IPO worth.

Nonetheless, they provide a weaker information to what occurs after the primary burst of demand is stuffed and public-market traders start deciding whether or not a valuation close to $1.8 trillion leaves sufficient room for error.

Regulatory scrutiny follows SpaceX’s IPO

In the meantime, the dimensions of the itemizing has drawn scrutiny in Washington, the place Sen. Elizabeth Warren has urged the Securities and Alternate Fee (SEC) to delay the providing till regulators handle dangers to retail traders and market construction.

Warren, the highest Democrat on the Senate Banking Committee, warned SEC Chair Paul Atkins {that a} SpaceX itemizing of this measurement may create uncommon dangers for public markets. Her considerations give attention to valuation, shareholder rights, and the corporate’s governance construction.

The letter argued that public traders could possibly be uncovered to an organization by which management stays closely concentrated amongst Musk and insiders.

Based on the lawmaker, supervoting shares, obligatory arbitration provisions, and Texas company legislation may restrict exterior shareholders’ capacity to problem administration choices or search authorized cures in disputes.

Warren additionally raised considerations about passive traders. At a valuation close to $1.8 trillion, SpaceX would probably change into a serious part of market indexes after itemizing. That would drive hundreds of thousands of traders in index funds and retirement accounts to achieve publicity to the corporate even when they by no means selected to purchase SpaceX instantly.

In view of this, Warren acknowledged:

“These will not be regular circumstances: quite a few further components exacerbate considerations and require motion by the SEC to fulfill its investor safety and market integrity mandates by delaying the [SpaceX] IPO.”

The warning provides a political layer to an providing already outlined by uncommon scale and retail consideration. It doesn’t imply the IPO shall be delayed. Registration supplies have moved by means of the SEC course of, and underwriters are getting ready for a debut that might change into probably the most intently watched market occasions in years.

Nonetheless, Warren’s intervention offers skeptics a transparent framework for questioning the deal. The considerations are not restricted as to whether SpaceX opens larger than $135.

They now prolong as to whether unusual traders perceive the authorized, governance, and valuation dangers embedded within the providing.