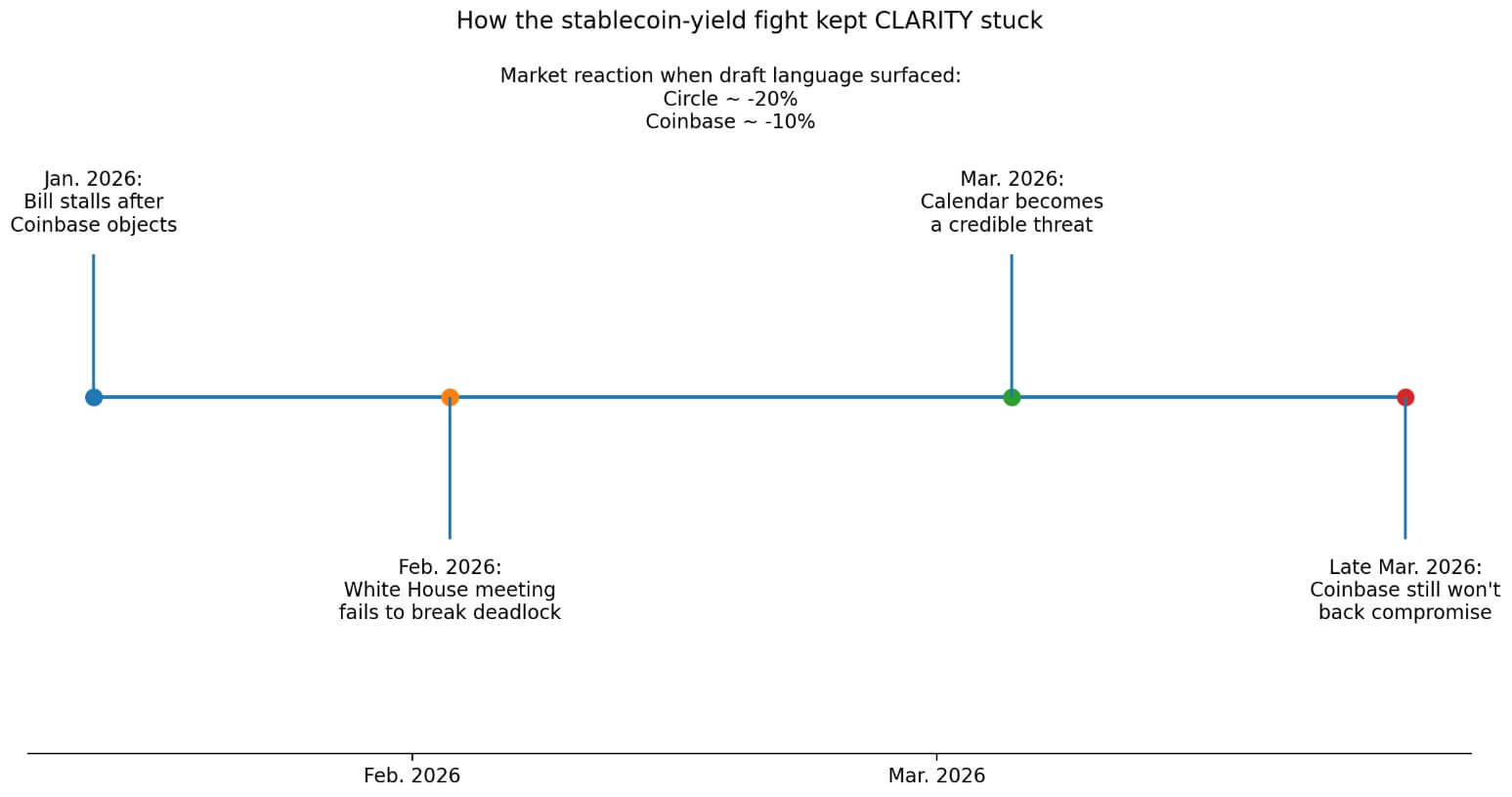

The stablecoin yield combat has as soon as once more consumed the CLARITY Act debate on Capitol Hill, and the price of that consumption is now measurable.

The invoice stalled in January when Coinbase objected to its phrases, a White Home assembly in February failed to interrupt the impasse, and by March, the calendar itself had change into a reputable risk to passage.

Punchbowl’s newest report steered Coinbase representatives advised the Senate they nonetheless couldn’t assist the latest stablecoin-yield compromise. However the sign is much less definitive than January’s break: Brian Armstrong has not publicly restated his opposition to the brand new textual content, and White Home crypto adviser Patrick Witt dismissed claims that Coinbase was as soon as once more blocking the invoice as “uninformed FUD.”

That leaves the reside query barely narrower than a full trade walkout: whether or not the most recent rewards language continues to be too restrictive to carry the coalition collectively on a invoice whose stakes run far past yield.

Banks need CLARITY to shut what they see as a loophole in final 12 months’s stablecoin legislation that lets exchanges pay passive rewards on idle balances. Crypto companies argue that banning rewards is anti-competitive and weakens person acquisition.

Circle fell roughly 20%, and Coinbase about 10% when draft language surfaced that will bar passive stablecoin rewards, indicating that markets are pricing this combat aggressively.

The combat considerations only one product function in a single class of balances. CLARITY’s attain extends throughout your entire US crypto working atmosphere.

The jurisdictional prize

In January, reviews famous that the Senate invoice would outline when tokens are securities, commodities, or in any other case, and grant the CFTC authority over spot crypto markets.

Senate Banking Republicans describe this as drawing a “shiny line” between the SEC’s and the CFTC’s jurisdiction, ending the enforcement-by-litigation regime that has ruled token classification for years.

The Home-passed framework assigns the CFTC core authority over registered digital commodity exchanges, brokers, and sellers, in addition to spot market contracts of sale.

That jurisdictional settlement underpins change listings, token distribution, institutional custody selections, and the authorized posture of each crypto agency working within the US at present.

Part 202 of the Home-passed textual content creates an exemption from conventional securities registration for qualifying digital commodity choices, supplied issuers meet disclosure necessities.

Sections 203-205 govern secondary market remedy, insider and affiliate gross sales, and the purpose at which a blockchain community qualifies as sufficiently “mature” to exit securities classification.

Senate Banking Republicans body this as a purpose-built disclosure regime that lets accountable tasks elevate capital whereas defending traders.

{kind=link}

For the subsequent era of builders, entry to a lawful US fundraising path carries extra long-run weight than any reward charge on a stablecoin steadiness.

| Space | What CLARITY would do | Why it issues |

|---|---|---|

| SEC vs. CFTC jurisdiction | Attracts a statutory line between when tokens fall below securities oversight and once they fall below digital commodity oversight, whereas giving the CFTC authority over spot crypto markets | Determines who regulates tokens, exchanges, and spot buying and selling, changing years of ambiguity and enforcement-driven classification |

| Token fundraising path | Creates a disclosure-based exemption for qualifying digital commodity choices and units guidelines for secondary-market remedy, insider gross sales, and when a community is taken into account “mature” | Provides tasks a lawful U.S. path to boost capital as an alternative of pushing token formation offshore |

| Developer and DeFi protections | Excludes sure actions corresponding to validating, node and oracle operation, publishing or updating software program, creating wallets, offering person interfaces, and publishing blockchain methods from being handled as regulated intermediation | Narrows authorized threat for builders and attracts a clearer line between writing code and working a monetary middleman |

| Self-custody and peer-to-peer rights | Preserves the fitting of people to make use of {hardware} or software program wallets for lawful self-custody and to have interaction in lawful peer-to-peer digital asset transactions | Protects primary possession and utilization rights that many in crypto view as foundational |

| Centralized market plumbing | Requires exchanges, brokers, and sellers to register, meet capital and risk-management requirements, segregate buyer funds, comply with surveillance and disclosure guidelines, and use certified custodians | Creates the operational and custody framework establishments want earlier than increasing U.S. crypto participation |

Builders, interfaces, and the code-versus-control line

Sections 309 and 409 of the Home-passed invoice exclude sure DeFi-related actions from SEC and CFTC regulation, whereas preserving anti-fraud and anti-manipulation authority.

The protected checklist consists of validating, node and oracle operation, publishing and updating software program, creating wallets, offering person interfaces, and publishing blockchain methods.

Senate Banking Republicans summarize the philosophy as regulating management. That framing carries direct weight for builders now working below real felony ambiguity.

A jury convicted Roman Storm in August 2025 on one rely of conspiracy to commit an unlicensed money-transmitting enterprise, tied to Twister Money. It deadlocked on the cash laundering and sanctions counts.

Prosecutors sought a retrial on the remaining costs.

Storm’s prosecution runs on a authorized monitor ruled solely by current legislation and alleged conduct predating any statutory reform.

A statute that treats publishing software program and working interfaces as protected exercise would draw a distinct line from the one prosecutors utilized in that courtroom, shaping the authorized publicity of the subsequent developer going through an analogous query.

The Home report states {that a} US particular person retains the fitting to keep up a {hardware} or software program pockets for lawful self-custody and to have interaction in direct peer-to-peer digital asset transactions for lawful functions, topic to sanctions and illicit-finance limits.

Senate Banking Republicans individually verify the invoice preserves self-custody. That provision addresses a foundational query about American crypto possession that solely a statute can settle with sturdiness throughout administrations.

The plumbing that establishments really need

Registered digital commodity exchanges below CLARITY must meet itemizing requirements, commerce surveillance obligations, conflict-of-interest guidelines, and system safeguards. They might checklist solely belongings with public disclosures masking supply code, transaction historical past, and asset economics.

Brokers and sellers would register, meet capital and risk-management requirements, segregate buyer funds, and maintain buyer digital belongings with certified custodians.

That is the layer of market infrastructure that enormous asset managers want earlier than increasing their US crypto publicity past already-approved ETF buildings.

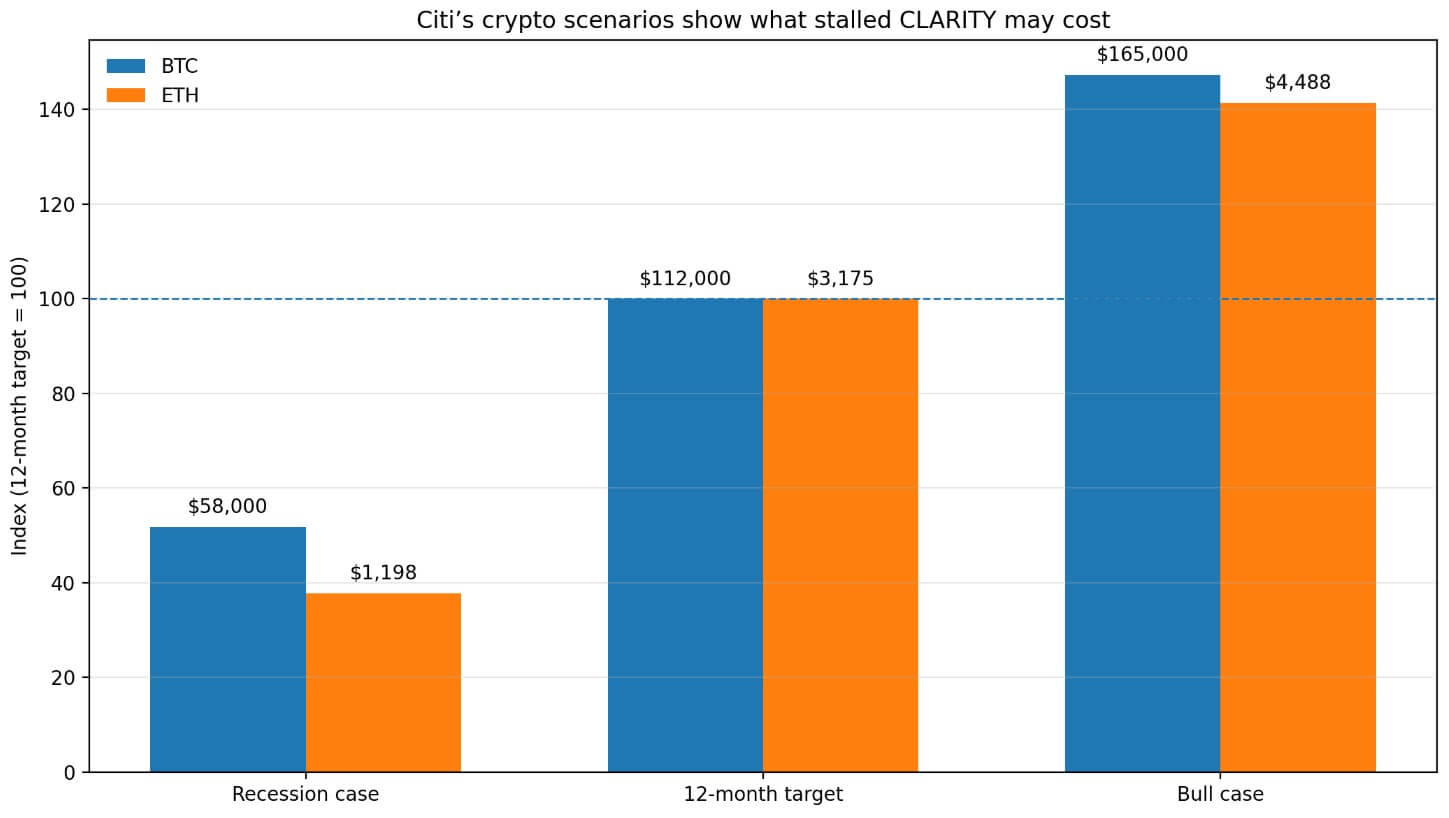

Citi lower its 12-month BTC goal to $112,000 from $143,000 and its ETH goal to $3,175 from $4,304 in March, citing stalled US market-structure laws and a narrowing window for the regulatory catalysts required for institutional adoption.

Citi’s bull case saved BTC at $165,000 and ETH at $4,488, and its recession state of affairs put BTC at $58,000 and ETH at $1,198.

That unfold between outcomes displays precisely what CLARITY was presupposed to compress: the uncertainty premium embedded in US token classification, change oversight, and institutional entry.

With no sturdy statute, the trade continues to function below company steering that shifts with administrations.

What to anticipate

A bullish conclusion consists of the yield combat discovering a workable compromise earlier than Senate ground time evaporates. With that veto level cleared, sufficient Democrats be a part of the coalition, and CLARITY reaches a remaining vote in 2026.

The market consequence runs immediately by means of Citi’s bull-case math: statutory SEC/CFTC strains revive the regulatory-catalyst narrative, giving institutional allocators the authorized certainty to develop positions.

Tasks launch US token choices below Part 202, developer legal responsibility narrows to conduct alone, and self-custody protections are embedded in federal legislation.

On the flip aspect, passive rewards and activity-based rewards might keep irreconcilable. Senate ground time would then bleed into ethics disputes, cross-committee reconciliation fights, and the midterm calendar.

Congress then approaches the elections and not using a finalized bundle, and crypto continues to function below enforcement historical past, partial company steering, and administration-dependent alerts.

As a consequence, the developer-liability query stays open, the SEC/CFTC boundary stays contested, tasks proceed to route capital raises offshore, and self-custody rights stay unprotected by statute.

The yield combat consuming CLARITY’s legislative window blocks the authorized structure that will govern who regulates tokens, how builders elevate cash, whether or not builders face felony publicity for publishing code, and whether or not People can maintain their very own belongings with out federal ambiguity.

Yield continues to be the clearest operational choke level, however it’s now not the invoice’s solely drag. Democrats concerned within the talks have additionally pushed conflict-of-interest and personal-profit considerations tied to Trump-linked crypto exercise, including one other supply of delay because the legislative window tightens.